Summary

Across the country, more small businesses report reopening and have cautious optimism about the future despite concerns about a resurgence of the coronavirus according to the latest MetLife & U.S. Chamber of Commerce Small Business Coronavirus Impact Poll.[1]

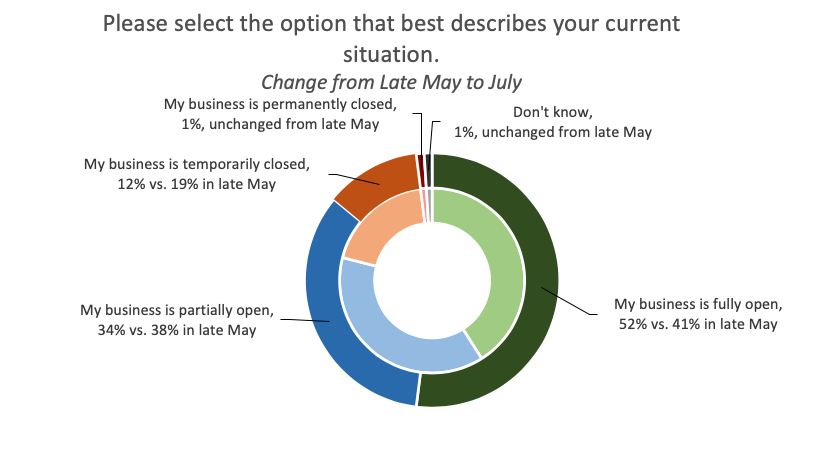

The survey focused on the ongoing impact from the coronavirus. This month, more small businesses say they are open, mostly due to an increase in businesses saying they are fully open. Small businesses that temporarily closed at some point since the pandemic began are more likely to say that they reopened this month (69%) than in late May (43%). This month, 86% of small businesses surveyed report they are either fully (52%) or partially (34%) open, up seven points from 79% in May.

Still, most small businesses are concerned about financial hardship due to prolonged closures (70%) and more than half worry about having to permanently close (58%). This month, more expressed concern over the lack of guidance on proper reopening procedures, up eight percentage points from late May (56% vs. 48% in May).

Though small businesses are pressing onward, concern over a second wave remains high. Two-thirds of small businesses (65%) are concerned about having to close again or stay closed if there is a second wave of COVID-19. Concern is particularly high among small businesses that already had to temporarily close (85%). The most common actions taken to prepare for a second wave are purchasing additional supplies or products to prevent a future shortage (32%), updating websites or social media profiles (29%), and increasing e-commerce or digital payment options (25%).

When it comes to the economy, perceptions of the national economy have steadied after declining sharply earlier this year. Though the overall number saying the national economy is in poor health is unchanged, slightly more say it is “very poor” compared to late May (24% now vs. 18% then). At the other end of the spectrum, 28% say the national economy is “good” (statistically similar to 24% who said the same in May).

Fewer small businesses perceive their local economy as in poor health (39%) when compared to the national economy (55%). Overall, small business views of the local economy are steady: 31% view their local economy as in “good” health compared to 28% in May. 39% see the local economy in “poor” health, statistically unchanged from May (38%).

55% of small businesses report good overall health, statistically similar to what was seen in late May (53%). In comparison, 65% reported being in good health in the first quarter of this year.

Comfort with cash flow holds steady this month (55% reporting comfort now versus 56% late May), although significantly below historical readings (above 80% in each quarter of 2019).

Over the long term, small businesses show signs of guarded optimism, but feel it will be some time before things return to normal. More than half of small businesses believe it will take six months to a year before the small business climate returns to normal (56%), in line with late May’s 55%. Another 7% think that it will never return to normal.

More than half expect next year’s revenues to increase (53% vs. 50% in May and 47% in April), while 18% expect them to decrease. Small businesses are now more likely to report plans to increase investments in the upcoming year (35%), up eight percentage points from May.

Staffing levels are in flux. 60% of small businesses report maintaining the same size staff over the last year (down from 67% in May), 20% report increasing staff over the same period (up from 13% in May), and 17% report decreasing staff during that time (similar to 18% in May). However, hiring expectations are somewhat improved: More small businesses anticipate increasing staff in the next year, up seven percentage points (30% versus 23% in late May).

Index Highlights

Almost 90% report their businesses are open in some capacity. 23% of small businesses report having temporarily closed at some point, unchanged from the end of May. In total, 86% of small businesses report that they are fully or partially open.

Services and retail slightly more likely to remain closed. By sector, slightly fewer services and retail businesses are open (82% each) compared to manufacturing (87%) and professional services firms (92%).

Businesses remain concerned about the impact of a second wave of coronavirus. 65% of businesses are concerned about having to close their business, or stay closed, if there is a second wave of COVID-19.

Majority of small businesses report actively preparing for resurgence of coronavirus. The most common preparatory actions include purchasing additional supplies to prevent shortages, updating their website and/or social media profile, and increasing e-commerce or digital payment options.

PPP loan recipients concerned about loan forgiveness. One in five (19%) respondents report applying for, and receiving, a PPP loan. Among loan recipients, nearly two-thirds (64%) are concerned about meeting the criteria necessary to receive loan forgiveness.

Those who laid off employees see months before they can rehire. Small businesses are more likely to report having fewer employees (21%) than more (11%) when compared to before the pandemic began. Among those with less employees, 48% say it could be anywhere from three months to a year before they anticipate rehiring most of their employees.

Long-term hiring expectations on the rise. However, more small businesses expect to increase staff in the next year compared to last quarter (30% now, versus 23% in May).

More plan to increase investment next year. 35% of small businesses report plans to increase investments in the upcoming year, up eight percentage points from late May. This is nearly double the number that report plans to reduce investments (18%).

Competition on the rise. Nearly one in three (31%) small businesses report facing more competition from smaller or local companies compared to six months ago—a 10 point increase from late May.

Spotlight: The Impact of the Coronavirus on Small Business

MAJORITY OF SMALL BUSINESSES PREPARING NOW FOR VIRUS RESURGENCE

Despite nearly eight in ten small businesses saying they are concerned about the pandemic’s impact on their business, more small businesses say they are open this month. Small businesses that temporarily closed at some point since the COVID-19 pandemic began (23%) are more likely to say that they reopened this month (69%) than in late May (43%).

In light of recent spikes in coronavirus cases, a majority of small businesses report taking action to prepare for a second wave of COVID-19. Widespread concerns persist this month regarding financial losses, more closures if there is a second wave, the risk the virus poses to their employees and customers, and a lack of guidance on safe operations.

ALMOST ALL SMALL BUSINESSES REPORT REOPENING IN SOME CAPACITY

Just as was seen in late May, 23% of small businesses report temporarily closing their business entirely since the start of the COVID-19 pandemic. This month, however, 86% report they are either fully (52%) or partially (34%) open (up seven points from 79% in May). For small businesses that reported a temporary closure at some point since the start of the COVID-19 pandemic (23%), most have reopened (69%). This is up from the 43% in May who said they had reopened.

Compared to previous surveys, there has been little change in the types of operational changes small businesses are making to deal with COVID-19. The most common responses remain shortening hours of operations and adjusting employee salaries or hours (30% and 29%, respectively, have done so at any point since the start of the pandemic).

Current operating status varies by sector, region and business size, as the below table shows. Virtually all small businesses with 20 employees or more report being open in some capacity, a 20-point increase from late May.

Most small businesses[2] are concerned about the financial hardships due to prolonged business closure (70%), and more than half worry about having to permanently close their business (58%). Three in five are concerned about the risks COVID-19 poses to customers and employees with reopening. More this month expressed concern over the lack of guidance on proper reopening procedures, up eight percentage points from late May (56% vs. 48% in May).

Most small businesses say they have the same number employees as in February of this year (67%). Moreover, small businesses are more likely to report having fewer employees (21%) than more (11%) when compared to before the pandemic began in the United States. Among those with less employees, 48% say it could be anywhere from three months to a year before they anticipate rehiring most of their employees.

The largest small businesses (those with 20-499 employees) are most likely to report staffing changes since earlier this year. Just 40% report having the same number of employees as they did pre-pandemic, with 26% saying they now have more employees and 33% saying they have fewer employees. They also are more pessimistic about bringing employees back, with 63% saying it will be longer than two months and 14% saying they do not anticipate rehiring at all.

In addition, 66% of small businesses agree that minority-owned small businesses have been disproportionately impacted by COVID-19.

CONCERNS OVER A SECOND WAVE OF VIRUS REMAINS HIGH

Though small businesses are pressing onward, concern over a second wave remains high. Two-thirds of small businesses (65%) are concerned about having to close again or stay closed if there is a second wave of COVID-19.[3] Concern is particularly high among small businesses that already had to temporarily close (85%), those in the South (72%), and those in the service industry (72%).

The most common action taken to prepare for a second wave3 is purchasing additional supplies or products to prevent a future shortage (32%), followed by updating websites or social media profiles (29%). A quarter report increasing e-commerce or digital payment options, and 13% report investing in accounting software. While around one in five small businesses report revisiting long-term staffing plans (18%), fewer have made plans for future layoffs or furloughs (12%) or already laid off or furloughed employees (9%).

Altogether, though, three in ten small businesses (31%) have not done anything from a list of options to prepare for a second wave of COVID-19. In states that have seen recent surges in cases,[4] more small businesses are taking preemptive measures (26% have not done anything on the list compared to 39% in all other states). Additionally, those who express concern about having to close for a second wave are more likely to report doing something to prepare (23% have not done anything compared to 44% of those who are not concerned about having to close due to a second wave).

MAJORITY SEE AT LEAST SIX MONTHS BEFORE BUSINESS RETURNS TO NORMAL

More than half of small businesses believe it will take six months to a year before the U.S. small business climate returns to normal (56%), in line with late May’s 55%. Another 7% think that it will never return to normal.

Small businesses in the South are most optimistic, with 45% saying that it will take less than six months (42% say six months to a year). Across industries, those in service are more likely to predict a longer return to normal: just 12% say under six months (down from 26% in late May), 65% say six months to a year (59% in late May), and 14% say the small business climate will never rebound (up from 3% in late May).

For small businesses that have not shut down entirely, most believe they can continue to operate without permanent closure for six months or more (53%). Manufacturing small businesses are least likely to think they can operate indefinitely (22%), followed by retail (30%). Those in service (37%) and professional services (40%) are far more likely to express confidence.

Current operating status could be linked to a business believing they can operate indefinitely without shutting down. Nearly half of small businesses that are currently open think they can operate indefinitely (45%), whereas those that are only partially open are half as likely to say this (22%).

As small businesses reopen, adaptations are being made.[5] As was seen in late May, the most common planned or implemented adaptation is more frequent cleaning of surfaces (50% vs. 48% in May). This is followed by requiring six feet of distance between employees and customers (42%), asking employees to stay home if feeling ill (41%), and requiring employees to wear protective gear (38%). Those who are not concerned about having to close due to a second wave are far more likely to say they have not made or plan to make any adaptations (27%), while those who are concerned are more likely to say they have made one of the listed adaptations (4% say they’ve not made, or plan to make, adaptations).

ONE FIFTH OF SMALL BUSINESSES REPORT RECEIVING A PPP LOAN

One in five (19%) small businesses have applied for and received a Paycheck Protection Program (PPP) loan. In total, 39% of small businesses have applied, or tried to apply, for a PPP loan. This includes those who have applied for a loan but did not receive it (9%), those who tried to apply but were unsuccessful (11%), and those who applied for and received a loan (19%). Altogether, fewer small businesses this month say they have not applied for the loan (49%) compared to late May (58%).

Small businesses who have not received the loan after applying (9% who applied but did not receive it and 11% who tried but were unsuccessful) are far less likely to say that they could continue operating indefinitely without permanently shutting down. Just 12% say this, compared to 31% of those who applied for and received the loan.

For the federal government to grant PPP loan forgiveness, small businesses must meet certain criteria regarding payroll and its costs. 64% of those who applied for and received the PPP loan are concerned about meeting these necessary criteria for loan forgiveness.

KEY FINDINGS:

SMALL BUSINESS OPERATIONS

CASH FLOW WOES PERSIST

Small businesses report their overall health holding steady. This month, 55% report good health (statistically unchanged from 53% late May).

This month, manufacturing (65%) and professional services (67%) are the most likely to report good health, while those in retail (45%) and service (40%) remain the least likely. As was seen in late May, small businesses in the Northeast (56%) and South (62%) are the most likely to report good health (47% in the Midwest and 50% in the West).

The smallest businesses (less than five employees) remain the least optimistic by size with just 43% reporting good health. While small businesses with more than 20 employees are just as optimistic as in late May (72% vs. 71% in May), mid-sized small businesses (5-19 employees) are now more likely to report good health (73% vs. 64% in May).

Comfort with cash flow remains unchanged from the end of May, with 55% of small businesses reporting comfort (56% in May). Small businesses across all regions have not seen dramatic differences in comfort with cash flow compared to late May. Historically, these levels of cash flow remain substantially lower than the norm: in each quarter of 2019 cash flow comfort remained above 80%. At the sector level, retailers’ and professional service firms’ comfort with their cash flow remains steady. Manufacturers are more optimistic than in late May (a 13-percentage point increase), while those in the service industry are less so (a 10-percentage point decrease).

More small businesses this month report spending more time on licensing, compliance or other government requirements in the last six months. Those spending more time has increased by eight points (29% vs. 21% in late May). Interestingly, those who received a loan through the Paycheck Protection Program (PPP) are more likely to report spending more time on compliance (35%) compared to those who have not applied for a PPP loan (22%).

SMALL BUSINESS ENVIRONMENT

MORE SEE INCREASED LOCAL COMPETITION

Twenty-nine percent of small businesses believe the U.S. economy is in good health, a slight, but not significant increase, from late May (24%). Though the overall number saying the national economy is in poor health is unchanged, slightly more say it is ‘very poor’ compared to late May (24% now vs. 18% then).

Fewer small businesses perceive their local economy as in poor health (39%) when compared to the national economy (55%). Overall, small business views of the local economy are steady: 31% view their local economy as in “good” health compared to 28% in May. The number that feel their local economy is in “poor” health is the same as in May (38%).

Nearly one in three small businesses (31%) report facing more competition from smaller or local companies, compared to six months ago—an increase of 10 percentage points since the end of May. Across regions, those in the Northeast and South are most likely to report more competition and both experienced double-digit increases for this measure since late May (17 and 13 points, respectively). Retailers are most likely to report this across industries (47% now, from 23%), and minority-owned businesses are more likely to report this than non-minority-owned businesses.

SMALL BUSINESS EXPECTATIONS

MORE REPORT LONG-TERM PLANS TO INCREASE INVESTMENT, STAFFING

This month, small businesses remain optimistic about future revenues, continuing the slight (but not statistically significant) upward trend seen in May (53% vs. 50% in May and 47% in April). Nearly three times more small businesses expect to see an increase (53%) rather than a decrease in next year’s revenues (18%).

Small businesses are more likely this month to report plans to increase investment in the upcoming year (35% vs. 27% in late May). Currently, nearly twice as many businesses plan to increase investments (35%) compared to those who are anticipating a reduction (18%).

Compared to late May, more small businesses in manufacturing, retail, and professional services are reporting plans to increase investments in the upcoming year. At the same time, small businesses in the service industry have become slightly less optimistic.

Though staffing levels are currently in flux for some due to COVID-19, long-term staffing expectations look more positive than last quarter. More small businesses anticipate increasing staff in the next year, up seven percentage points (30% vs. 23% in late May). Half plan to retain the same staffing size (53% vs. 60% in late May) and just 9% report plans to reduce staff (10% in late May).

U.S. Chamber Resources for Small Businesses

For small business resources on the coronavirus, visit www.uschamber.com/co.

- Step-by-step guidelines on applying for a loan through the Paycheck Protection Program are available at www.uschamber.com/sbloans.

- A guide to the Small Business Administration’s expanded Economic Injury Disaster Loan Program (EIDL) program to assist small businesses is available at www.uschamber.com/report/guide-sbas-economic-injury-disaster-loans.

- A guide to CARES Act Relief for independent contractors or those who are self-employed and don’t have any employees is available at www.uschamber.com/report/independent-contractors-guide-cares-act-relief.

Survey Methodology

The sample for this study was randomly drawn from Ipsos’ online panel, partner online panel sources, and “river” sampling and does not rely on a population frame in the traditional sense. Ipsos uses fixed sample targets, unique to the study, in drawing sample. Small businesses are defined in this study as companies with fewer than 500 employees that are not sole proprietorships. Ipsos used fixed sample targets, unique to this study, in drawing sample. This sample calibrates respondent characteristics to be representative of the U.S. small business population using standard procedures such as raking-ratio adjustments. The source of these population targets is U.S. Census 2016 Statistics of U.S. Businesses dataset. The sample drawn for this study reflects fixed sample targets on firmographics. Post-hoc weights were made to the population characteristics on region, industry sector and size of business.

Statistical margins of error are not applicable to online non-probability polls. All sample surveys and polls may be subject to other sources of error, including, but not limited to coverage error and measurement error. Where figures do not sum to 100, this is due to the effects of rounding. The precision of Ipsos online polls is measured using a credibility interval. In this case, the poll has a credibility interval of plus or minus 5.0 percentage points for all respondents. Ipsos calculates a design effect (DEFF) for each study based on the variation of the weights, following the formula of Kish (1965). This study had a credibility interval adjusted for design effect of the following (n=500, DEFF=1.5, adjusted Confidence Interval=+/-6.5 percentage points).

[1] Beginning in Q2 2020, the MetLife/U.S. Chamber of Commerce Small Business Index survey has been conducted via a monthly online survey, in place of the typical phone-based approach. This methodological shift is in response to anticipated lower response rates in dialing business locations as a result of mandated closures related to the COVID-19 outbreak. While significant changes in data points can largely be attributed to the recent economic environment, switching from a phone to online approach may have also generated a mode effect.

[2] Note: the 1% of businesses that report being permanently closed were not asked this question.

[3] Note: the 1% of businesses that report being permanently closed were not asked this question.

[4] States experiencing recent surges include Connecticut, New York, New Jersey, Arizona, Florida, Georgia, Texas, Pennsylvania, Ohio, Michigan, Wisconsin, Indiana, California, Oregon, and Washington.

[5] Note: the 1% of businesses that report being permanently closed were not asked this question.