Key Takeaways

- 57% of middle market executives are expecting an increase in both gross revenues and net earnings through the middle of the year.

- 53% said they had bolstered their stock of goods, which, given the drawing down of excess savings by households, demands close monitoring.

- Middle market business conditions remain solid heading into the middle of the year as firms continue to adapt, improvise and overcome challenges.

A resilient American economic expansion is continuing in the middle market as firms navigate economic headwinds and crosscurrents, according to a recent survey of executives by RSM US LLP.

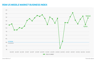

Easing inflation and solid household consumption underscored the 9.4-point increase in the RSM US Middle Market Business Index, which saw the top-line figure jump to 134.0 in the first quarter from 124.6 during the final three months of last year. The survey was conducted from Jan. 9 to Jan. 30 and reflects the responses of 406 senior executives at middle market firms across industries.

“With a 9.4-point increase in topline sentiment, middle market firms have optimism about business conditions as we start the year. Increases reported in firms’ revenues and earnings for Q1 2023 and slowing inflation are driving optimism in the middle market sector. However, as household savings continue to fall, close attention will have to be paid to consumers’ ability to spend throughout the year and the impact of a potential decrease in household expenditures.”

-Neil Bradley, executive vice president, chief policy officer and head of strategic advocacy at the U.S. Chamber of Commerce

If one had asked a year ago whether the American real economy would be able to absorb the twin shocks of surging inflation and rising interest rates, the prevailing consensus would have almost certainly been no.

For now, though, that is not the case. The economy expanded at a 3% pace during the final six months of last year, and robust consumer activity in January indicates that the current economic expansion is not finished.

The ability of the middle market to withstand those hits reflects an underlying resilience of households and midsize organizations to adapt to the unique crosscurrents that characterize the post-pandemic economy.

The increase in the top-line index reflects not only that resilience but also relief. Overall inflation peaked last June, continues to moderate and is experiencing outright disinflation in the goods sector.

This has influenced the 53% of respondents who indicated an increase in gross revenues, up from 42% in the final quarter of last year, and the 49% of participants who reported an increase in net earnings.

More impressive is the forward look of the 57% of respondents who are expecting an increase in both gross revenues and net earnings through the middle of the year.

But that combination of resilience and relief has also bolstered business confidence to the point that firms are increasing inventories in the first quarter, posing a degree of risk going forward as the lagged impact of interest rate increases starts to sink in.

More than half, or 53%, of MMBI respondents said they had bolstered their stock of goods, which, given the drawing down of excess savings by households, demands close monitoring.

The recession question

The current pace of household consumption, with retail sales increasing by 3% in January, is likely unsustainable. An old-fashioned inventory overhang is one way to help put the economy into a recession.

We have previously made the case that we could see a mild recession instead of a slowdown if firms pull back on gross private investment.

That restraint was evident during the final three months of last year, when firms decreased fixed business investment by 6.7%, driven by a decline of 3.7% in outlays on equipment.

Residential investment dropped by 26.7% during the final quarter of 2022, and the housing sector is the one industrial ecosystem now in recession.

If the U.S. economy falls into a recession this year, it will most likely be an unsynchronized contraction, with housing, manufacturing and retail, as well as other areas of the service economy, experiencing it to different degrees.

But not all areas of the services sector will see similar adverse circumstances, so we maintain our baseline view on a mild recession this year.

The data

In the survey, sentiment on the overall economy surged, with 47% of executives indicating the economy had improved, up from only 28% previously, and 41% expecting it to improve over the next six months.

The combination of solid demand, an easing in prices paid and a mild increase in prices received is most likely behind a plurality of respondents indicating a general improvement in economic conditions.

Roughly 69% of respondents said that prices paid had increased, down from a recent peak of 82% in the third quarter of last year. Overall inflation peaked last June, and middle market firms have no doubt benefited from the correction in oil and gasoline prices. They have also been aided by disinflation in the goods sector, which is a big reason for the increase in top-line sentiment.

One note of caution: Service sector inflation has not yet peaked. It is up by 7.6% on a year-ago basis through January, mostly driven by housing and housing services. Both of those categories are part of a complex chain of factors driving rising wages.

Costs for core services excluding housing rose by 6.18% through the end of January. Both services costs and core services costs, excluding shelter, tend to be sticky, and will most likely not recede as quickly as goods prices as supply chain disruptions dissipate.

Demand at the start of the year was so strong that 55% of respondents indicated they benefited from an increase in prices received. Approximately 62% of respondents expect to pass along higher prices over the next six months.

Capital expenditures continue to impress, with 49% of respondents indicating that they had increased outlays on productivity-enhancing software, equipment and intellectual property in the quarter. A full 55% said they intended to do so through midyear.

Employment and compensation both continue to reflect a historically tight labor market that will most likely temper the robust gross revenues and earnings outlook.

Of firms surveyed, 47% increased hiring and 58% used higher compensation to attract labor. Looking ahead, 51% of respondents intend to hire more workers and 63% indicated they will increase compensation to compete for scarce labor.

The takeaway

Middle market business conditions remain solid heading into the middle of the year as firms continue to adapt, improvise and overcome substantial challenges posed by interest rate hikes and inflation.

UK MMBI posts dramatic jump

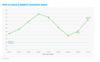

“The U.K. economy has shown remarkable resilience in the face of a record-breaking fall in real incomes and the largest rise in interest rates in a generation. The middle market is no exception. Indeed, the RSM UK Middle Market Business Index rose to 131.4 in Q1, a jump of almost 16 points, the largest in the index’s relatively short history.

“However, there are two key risks ahead. First, despite the recent resilience, the U.K. economy is still likely to fall into recession in the first half of this year. Second, there was a large jump in the proportion of middle market firms accumulating stocks (inventories). This increase in stock levels is particularly concerning because demand, especially for goods, is likely to decrease over the next six months as the real economy falls into recession.”

-Thomas Pugh, Economist, RSM UK

On the middle market mind

We asked middle market executives to describe a top business problem facing their organization. Here's what they had to say:

- Choosing the right technology. – Retail trade executive

- My organization's main future focus will be on labor and skill shortages. – Construction executive

- Financial management is one of the frequent business issues that our organization is now confronting. – Utilities executive

- Incorporating robotics and automation. – Manufacturing executive

- Budgetary constraints, lack of professional training and poor network infrastructure are the major challenges we have in our organization right now. – Educational executive

- It is critical to focus on inventory and project management. – Manufacturing executive

- Changing business models and customer retention are problems facing the organization. – Finance executive

- Hybrid work environment and cybersecurity threats are major problems in IT. – Information sector executive

- The major issue we have in our firm is outdated technology and supply chain security. – Retail trade executive

- Slow adaption to emerging technologies. – Construction executive

See more Middle Market Index data and visualizations at RSM's website.