“When elephants fight, it is the grass that suffers.” This African proverb is widely cited in Southeast Asia, where anxieties about U.S.-China relations have long run high, and even more so over the past couple years as the trade relationship has frayed. Not wanting to choose sides, and not wanting disruptive economic fallout from a U.S.-China rupture, countries in the region remain very concerned about the course of the two elephants’ relationship. And rightly so.

At the same time, it has been lost on no one that the trade conflict also presents opportunities for Southeast Asia. Starting in 2018, amid long-festering and unresolved trade disagreements with China, the United States applied four waves of tariffs (as high as 25%) against hundreds of billions of dollars-worth of Chinese products. These tariffs incentivized Chinese exporters and suppliers to the U.S. to find alternative production locations, including Southeast Asia. Countries in Southeast Asia responded, in some cases by actively courting outbound Chinese investment.

But how much has the region benefitted? With a full two years’ worth of trade data to assess, it’s now possible to begin drawing a picture.

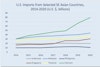

Many Southeast Asian countries grew their exports to the U.S. in the wake of the trade spat (see chart). Vietnam became the largest beneficiary in dollar terms. However, all the larger countries in the region (with the exception of Indonesia) have seen growth in their exports to the U.S. in recent years, both before and after the Chinese tariffs. The question is: How much of this is actually attributable to the China tariffs?

In order to better understand this, a recent U.S. Chamber of Commerce study created an “average tariff advantage” (ATA) to compare country-specific opportunities created by the China Section 301 tariffs.

Based on this formulation, Indonesia, Malaysia, Philippines, Thailand, and Vietnam had ATAs of between 13%-19%. Such hefty margins suggest that these countries should substantially increase their exports of the tariffed products to the U.S. For comparison, the world average ATA is 15%.

However, the data reveal some things you wouldn’t expect. First, the Philippines had the highest ATA of any Southeast Asian country, yet it saw very modest export growth to the U.S. At the same time, Vietnam had the lowest ATA in the region, but increased its exports to the U.S. (measured in dollars) more than other ASEAN countries. Perhaps this discrepancy is because some Southeast Asian countries do not export large amounts of tariffed products or do not have the capacity to do so at the volumes and standards required. In effect, they can’t quickly take advantage of their high ATAs.

Nonetheless, cost differentials have created opportunities for these countries to grow their U.S. market share. For example, Malaysia has been able to expand its exports of products including thermostats, telecommunications instruments, battery parts, and transistors and semiconductor parts. Thailand has seen strong growth in U.S.-bound exports of computers, storage devices, and medical instruments. These examples show the diversity of the region’s exports and suggests there are growth opportunities, particularly where ATAs are high.

Southeast Asian countries continue to enhance their laws and regulations to better compete for business opportunities created by the U.S./China tariffs. Indonesia recently passed reform legislation that opens up the economy more broadly to foreign investment and addresses longstanding manpower issues. The Philippines is close to enacting substantial tax reforms long championed by the business community. Thailand continues to promote a broad array of tax and other incentives to attract foreign investment. These countries are also pursuing a variety of bilateral trade agreements with partners around the globe.

The Biden administration has made it clear that it will not prioritize the removal of tariffs on certain Chinese goods. This provides a continuing opportunity for Southeast Asian countries to take advantage of their comparative edge, boost their competitiveness, and gain market share in products where tariffs are high, all of which, accompanied by an effective vaccine rollout, will support the region’s economic recovery. The elephants may continue to fight, but so far the grass is holding up well.

About the author

John Goyer

John Goyer is executive director of Southeast Asia at the U.S. Chamber of Commerce. Goyer focuses on issues of market access, investment barriers, regulatory and other issues that pose challenges for U.S. business in Southeast Asia.