A six-figure salary at a fast food restaurant sounds too good to be true. But in today’s tight labor market it is a reality. Taco Bell will soon pay some restaurant managers $100,000 a year. This is great news for workers, especially those with fewer skills. In fact, wages for the lowest paid workers are now growing faster than for higher-paid workers.

The cause of these wage gains for less-skilled workers is clear. The labor market is tight, which means there are fewer and fewer workers to fill open positions. Businesses have to pay workers more to either attract new employees or retain current ones. Simple, old fashioned supply and demand is driving wages up.

Wages are not rising because restrictive immigrations policies are limiting the number of available workers, as some have argued. Rather, the workers filling jobs now are those that have been on the fringes of the labor market during the recovery and are now fully rejoining the workforce because jobs are paying better.

The evidence of a tight labor market is abundant. The National Foundation of Independent Business’s Small Business Economics Trends survey has for several months now found that the number one concern of small businesses is finding qualified workers to fill available positions. More than half of all businesses find “few or no qualified applicants” for their job openings.

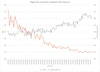

Additionally, the U.S. Chamber of Commerce’s Worker Availability Ratio (WAR), an analysis of the available workers in the U.S. compared to the number of job openings across the nation, hit a record low in October (the most recent month for which the data is available). There are now only 0.88 workers available for every open job. This means that if every unemployed person in the U.S. received a job, there would still be unfilled positions.

The ratio differs widely by state. In North Dakota the ratio is 0.51. The state would need almost twice as many workers as are available there to fill all the job openings.

As the nearby chart shows, the WAR has fallen wages have risen. Again, straight forward supply and demand is pushing wages higher.

When the economy began to grow again in June of 2009 after the 2007-2009 recession, wages grew faster for those at the top of the income distribution. It is only since 2017 that wage growth for those at the bottom has consistently exceeded higher-income groups.

That it would take longer for wages to grow at the bottom makes sense if you follow the data. In the aftermath of the economic crisis, the unemployment rate for those with more skills (using education levels as a proxy) fell by fewer precentage points than the unemployment rate for those with fewer skills. The unemployment rate for all workers with a bachelor’s degree or greater peaked at just 5% during the recession and its aftermath. It had been 2.1% before the recession. For high school graduates the peak was 11%. It had been 4.7% before the recession. For context, the highest unemployment rate for all workers was 10% during the recession.

As the recovery began, there were significantly more low-skilled workers available than there were higher-skilled workers. Businesses had to compete harder for the higher-skilled workers, so their wages grew faster. Unfortunately for lower-skilled workers it took about eight years, into 2017, for businesses to hire enough to reduce the pool of available low-skilled workers to the point where their wages shot up. Nevertheless, it eventually happened and continues through the present.

These higher wages are drawing people back into the labor force at a rapid pace. The labor force has grown by nearly 10 million since the recession ended, but about half that growth has occurred since the beginning of 2017 when wage growth at the bottom began accelerating. It is these workers flooding in to the labor market who are filling the available jobs. They are benefitting from having a job and from the higher wages those jobs are paying.

The expansion fortunately lasted long enough for this effect to take hold. A large portion of those 5 million workers that joined the labor force since 2017 might not have had the chance had the expansion ended earlier. This is an enormous added benefit of a prolonged expansion.

Some have argued that restricting immigration can play a role in keeping wages growing strongly for those at the bottom of the income scale by keeping the supply of lower-skilled workers down. However, there are only so many workers businesses can entice back into the labor market with higher wages. Labor force participation has been declining, regardless of economic conditions, because of the aging of society and the fewer prime age males working. We may soon hit a point where the labor force growth will tail off even as wages rise sharply. In this case, immigration will be necessary to fill available jobs.

Minimum wage increases in several states and some larger cities have contributed to higher wages for less-skilled workers. Ernie Tedeschi in a New York Times column finds that those increases caused 0.4 percentage points of the 3.9% increase of wages for the bottom third of the income scale the last two years. But the effect of supply and demand far outweighs this impact.

Rising inflation is a concern for some when wages rise quickly. However inflation is well-tamed and has been during the entire expansion. It is either just above, or slightly below, the Fed’s 2% target depending on the metric. There is little concern about it rising rapidly in the near future.

Furthermore, the surge in wage growth at the bottom of the income scale is the result of those workers finally sharing more fully in the benefits of the expansion. They are still catching up to other workers who have seen their wages grow faster and to wages levels they would have seen if not for the severe recession. Inflation will not be a factor unless these workers’ pay outpaces their productivity gains. We are not close to that level yet.

In fact, wages could grow faster for all workers without causing inflation if productivity, which has been up and down recently, would pick up consistently. Workers are more productivity when businesses invest more, but investment has declined in recent months. Businesses are skittish because of the uncertainty from trade disputes and other factors. If those concerns were addressed, businesses would start investing again, productivity would rise, and wages would rise even higher.

About the author

Curtis Dubay

Curtis Dubay is Chief Economist, Economic Policy Division at the U.S. Chamber of Commerce. He heads the Chamber’s research on the U.S. and global economies.